Executive Summary

January 2026 data points to a winter-season market where demand is active, but pricing remains disciplined and increasingly data-driven. In the Bonita/Estero micro-market, closed sales rose year-over-year while the median price eased—an important signal that more deals are getting done as buyers lean into leverage created by higher inventory.

Across the broader region, the late-2025 pattern of rising pendings alongside elevated supply frames January as part of an ongoing “rebalance” rather than a return to a 2021-style frenzy.

Seasonality still matters (winter visibility and buyer traffic), so the cleanest comparisons for trend are year-over-year, not month-to-month.

Key Metrics Snapshot

Market definition note: “Bonita/Estero micro-market” is treated as defined by the BER market reports dashboard.

Active Inventory

New Listings

Pending Sales

Closed Sales

Median Sale Price

Months of Inventory

Median DOM

Market Context and Comparisons

How January 2026 fits into the late-2025 “rebalance” arc

The most useful context for January 2026 is late 2025’s shift from “frenzy” to a competitive but negotiable market—more listings, longer marketing times, and buyers regaining choice.

In November 2025, the region saw pending sales rise to roughly 3,600 contracts (more than 20% year-over-year) while closed sales improved by around 6% versus November 2024, even as new listings were lower than the prior year—an absorption-friendly setup heading into winter.

January 2026’s Bonita/Estero snapshot aligns with that framing: higher closed-sale volume year-over-year, paired with a softer median price, suggests sellers are meeting the market to keep transactions moving. That is consistent with the broader 2024–2025 pattern described in our previous “market rebalance” analysis: volume can recover even when price growth is flat, provided rates stabilize and buyers have selection.

Seasonality and why YoY change is the lead indicator

Florida Realtors guidance embedded in local market reporting underscores that closed sales (and many related metrics) have seasonal cycles, making year-over-year comparisons the more reliable measure of trend versus month-to-month swings. Highlight YoY first, then use Nov→Jan comparisons as a “momentum check” (fall-to-winter ramp).

Baseline comparison to 2024 conditions

Our longer-form 2024–2025 market rebalance analysis describes a market where prices held well above pre-pandemic levels but stopped accelerating, inventory rebuilt substantially, and days on market returned toward “normal.”

This context supports a January 2026 narrative of “steadying” instead of “surging”—especially when paired with price softness in certain submarkets and elevated cash participation (a continuing feature of the region’s demand profile).

Drivers and Interpretations Behind January 2026 Conditions

Inventory and months of supply are still the leverage engine

The clearest structural driver from 2024–2025 into early 2026 is the inventory rebuild. The market-rebalance analysis notes that listings across Lee and Collier climbed into the ~18,600 range by late 2025, and months of supply moved closer to balanced levels (rather than the sub‑1‑month conditions of 2021).

That inventory normalization changes negotiation dynamics: it reduces urgency, increases price sensitivity, and raises the penalty for overpricing.

For additional regional texture, reporting derived from Florida Gulf Coast University economic indicators describes a “higher inventory + improving sales volume” environment in late 2025, with daily average active listings in November 2025 around 21,871 region-wide (Lee 11,692; Collier 6,174). While that is not January 2026 inventory, it is directly relevant context for why buyer leverage persisted into the winter season.

Interest rates and affordability: the “pressure valve,” not the whole story

The market rebalance article frames mortgage rates as a key swing factor: it cites a decline in the 30‑year fixed rate to about 6.19% in December 2025 after being near 7.33% in November 2025, describing how even modest rate relief can unlock pent-up demand.

This is a clean way to discuss January 2026: if buyers believe rates are stabilizing (or drifting down), they are more willing to go under contract—especially in mid-price segments.

At the same time, the regional analysis repeatedly emphasizes that cash remains a dominant force, meaning the market’s marginal buyer is often equity-driven. That is part of why prices “soften gently” instead of collapsing: demand is not solely mortgage-dependent.

Migration and seasonal presence: demand is still arriving “physically in-market”

Previous reporting on our website frames the 2020–2022 boom as migration-fueled and suggests the area’s desirability continues supporting price resilience even as the market cools. Separately, the RSW passenger record article argues that airport traffic is an early indicator of winter-season demand (visitor volume, second-home shopping, relocation trips), and it pairs that with higher inventory—an environment where more showings do not automatically translate to runaway bidding, but do support absorption.

New construction and data interpretation caveat

One technical nuance worth including in an analytical version of the article: in markets with meaningful new construction, “days on market” can be skewed if developments are entered into MLS as listings that go pending immediately (0–1 DOM), impacting averages. Since this piece cites DOM prominently, this is a responsible and confidence-building footnote when presenting DOM/absorption metrics.

Investor activity and “cash vs. financed” segmentation

The 2024–2025 rebalance article explicitly describes a two-tier market shaped by high mortgage rates: more cash participation and fewer first-time buyers, with investors and equity-rich households remaining active.

This January 2026 story interprets price softness alongside rising closings as evidence of more efficient price discovery rather than weakening demand: buyers transact when pricing matches the expanded set of alternatives.

When new listings exceed closings for extended periods, inventory builds; when closings catch up, inventory stabilizes.

Regional Commentary and Video Insights

Bonita/Estero micro-market: higher closings, softer median price

The BER market dashboard's January 2026 micro-market snapshot shows 242 closed sales (+19.2% YoY) and a $537,500 median sale price (‑6.5% YoY). That pairing supports the headline: “More deals are closing, but sellers are competing.” In practice, this often corresponds to (a) better-priced inventory winning quickly, (b) over-ambitious listings sitting longer, and (c) negotiated outcomes returning (inspection credits, concessions, or price reductions) as a normal part of high-season transactions.

Takeaways: Months of inventory decreased YoY to 9.1 months. Pendings outpaced new listings growth, indicating strong winter absorption despite competitive pricing needed from sellers.

Pendings are the lead indicator for closings; use them to describe momentum heading into the next 30–60 days.

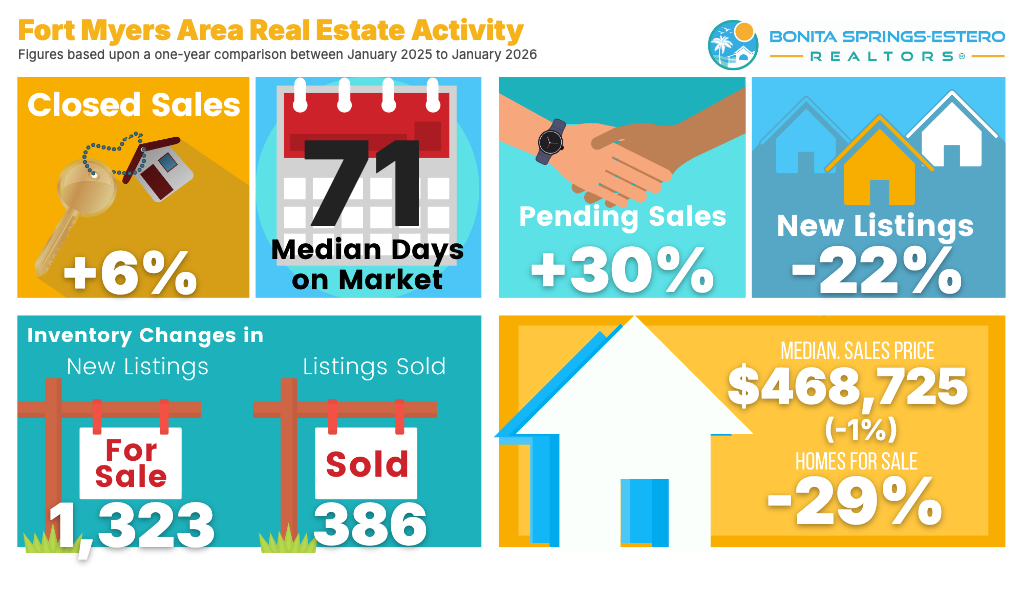

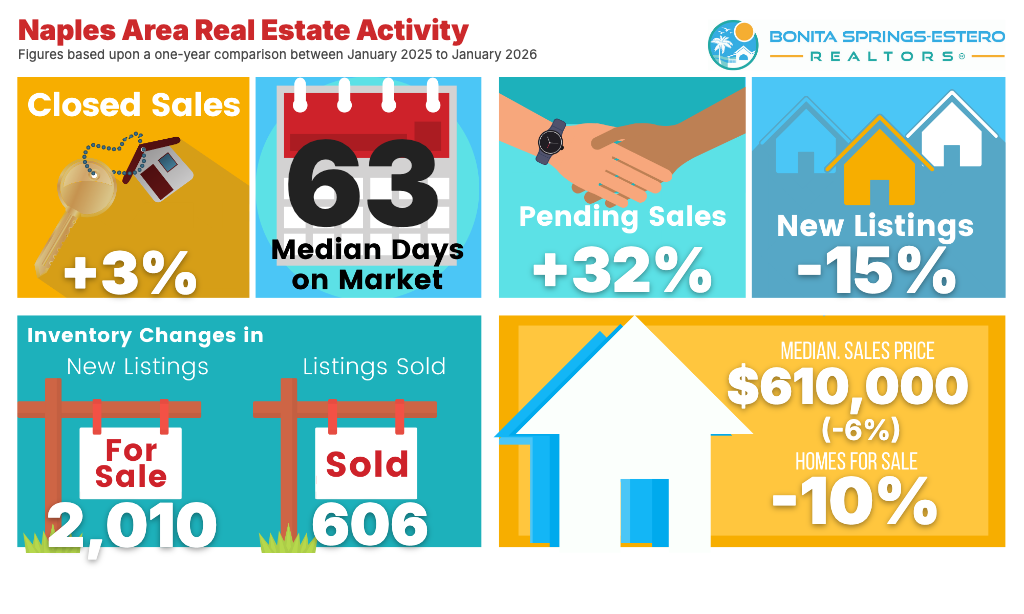

Fort Myers and Naples: stable pricing and rising pendings

In the surrounding major markets, Fort Myers is showing stability in average pricing around the mid-$400s. To the south, Naples reporting describes pending sales surging over 40% year-over-year, alongside a median closed price of $627,500 (‑4.1% YoY). The clean takeaway across both regions is that buyer activity is responding to competitive pricing, not disappearing.

Takeaways: Fort Myers maintains pricing stability while Naples experiences significant momentum in pending sales, showing that buyers remain highly active when sellers align their expectations with current market inventory.

Outlook and Actionable Advice

Three-to-six month outlook

The macroeconomic framing suggests that if rates stabilize or drift down, demand can “pop” and move the market closer to balance—especially in segments where buyers have been waiting for affordability relief. At the same time, inventory normalization is now a core feature of the market: the region is not operating under the “scarcity” regime of 2021, so a seller’s market is unlikely without a meaningful supply contraction.

“Expect continued high-season activity into early spring, with the strongest response in homes that are priced correctly relative to competing inventory and total carrying costs.”

- Watch pendings vs new listings as the early signal: if pendings consistently exceed new listings, months of inventory can compress and pricing can firm.

- If rates hover near the mid‑6% range, the market can remain “active but selective,” rather than reverting to bidding-wars as the default.

DOM reflects market tempo; interpret carefully in new-construction-heavy segments where 0–1 DOM entries can distort averages.

Actionable advice for buyers and sellers

For buyers: The best strategy in a “selection-rich” environment is to treat the market as a set of micro-markets and negotiate based on comparable competition, not headlines. The region’s own analysis emphasizes that buyers have more choices and can be choosier, which increases the value of disciplined underwriting and precise comps. Action: buyers act faster in tight subsegments; sellers hold firmer on top comps.

For sellers: The same analysis supports a clear operational message: pricing accuracy matters more than it did in the frenzy, and homes can take materially longer to sell, making preparation and early pricing adjustments the highest-leverage decisions. Action: price precisely, expect negotiation, optimize condition.

Data sources include Bonita Springs-Estero

REALTORS® dashboard, Florida Realtors, and Naples Area Board of REALTORS®.

For additional

context on the shift in the market over the last two years, see our 2024-2025 Market

Rebalance report.